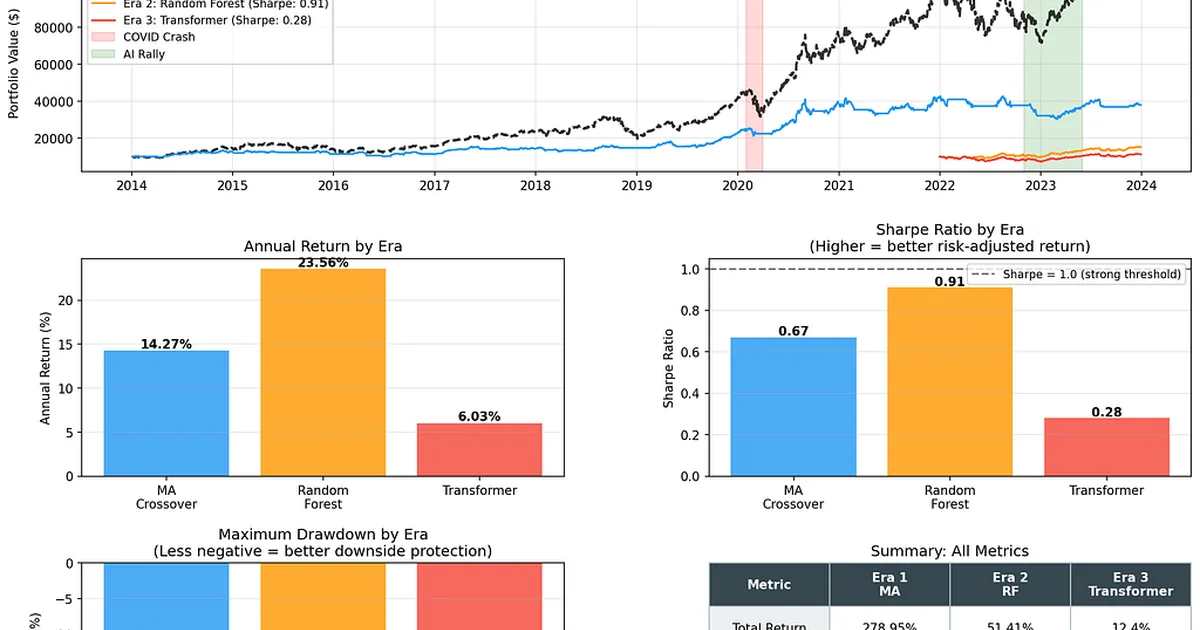

A recent research project compared three distinct eras of quantitative finance strategies—rule-based, classical machine learning, and deep learning—using 10 years of Apple stock data. Surprisingly, the most complex deep learning model, a Transformer architecture similar to those powering ChatGPT, performed the worst across all metrics. A 1990s-era Random Forest model achieved the best risk-adjusted returns, suggesting that market noise and overfitting can hinder the performance of highly complex models in financial applications. AI

IMPACT Suggests that simpler AI models may be more effective than complex deep learning architectures for financial time-series analysis due to market noise and overfitting.

RANK_REASON The cluster discusses a research project comparing different AI model types on financial data, including a reference to a published paper. [lever_c_demoted from research: ic=1 ai=1.0]

- Apple

- ChatGPT

- deep-learning model

- Ml Models

- PatchTST

- Random Forest

- Rule-based models of the interplay between genetic and environmental factors in childhood allergy

AI-generated summary · Google Gemini · from 1 sources. How we write summaries →