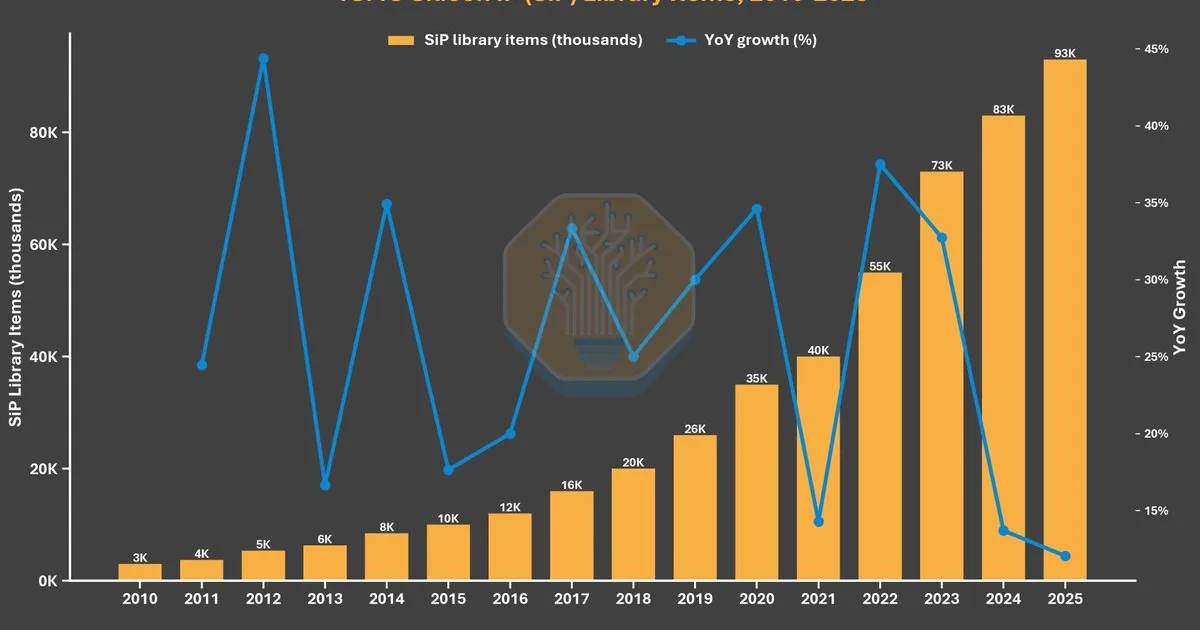

SemiAnalysis argues that TSMC's competitive advantage lies not in process technology (PPA, EUV, yield) but in its extensive Electronic Design Automation (EDA) and intellectual property (IP) ecosystem. This ecosystem, which has grown significantly over the years, includes numerous pre-qualified interface blocks and IP vendors. This comprehensive network reduces design risk and increases the cost for competitors like Samsung and Intel to lure away TSMC's customers, effectively creating a strong platform lock-in. AI

IMPACT Highlights how ecosystem lock-in, rather than just raw performance, shapes competition in semiconductor manufacturing.

RANK_REASON Analysis from SemiAnalysis discussing competitive moats in the semiconductor industry.

- ALPHAWAVE IP GROUP PLC

- Arm Holdings

- Cadence

- EDA/IP ecosystem

- extreme ultraviolet lithography

- Intel

- intellectual property

- Rambus

- Samsung

- SemiAnalysis

- Synopsys

- TSMC

AI-generated summary · Google Gemini · from 8 sources. How we write summaries →